MakerDAO and the future of DeFi

How MakerDAO is an early predictor of the changing face of DeFi

MakerDAO is one of the oldest and most successful apps in DeFi and also one of the most decentralized — but the banning of Tornado Cash and the politicization of USDC has raised profound existential questions about what it can do and what it should be. The debate about the future of MakerDAO is unfolding now, forcing the community to balance and prioritize censorship-resistance, scalability and stability. The choices they make will have profound implications not just for MakerDAO but for all of DeFi.

In this issue:

What is MakerDAO?

How SAI became DAI

Stability through compromise

Solve all your problems with YOLO

Where we go from here

What is MakerDAO?

MakerDAO is a smart contract that lives on the Ethereum blockchain and acts a bit like the halfway point between a bank and a vending machine. MakerDAO manages two tokens, MKR (a governance token that controls the contract) and DAI (a stablecoin pegged to the value of USD). Smart contract managed stablecoins have a bad reputation after the violent collapse of Terra/Luna but MakerDAO has a fundamentally different approach. The existential risks of MakerDAO are real but are also very different.

We’re going to start by describing single-collateral DAI, now known as SAI. Modern DAI is actually multi-collateral and works somewhat differently. More on that in a bit.

MakerDAO customers deposit ETH as collateral and receive a loan in DAI. Later they can repay their loans (plus interest) and retrieve their collateral. If the price of ETH drops too far before the loan is repaid the collateral is automatically sold to repay the loan. MakerDAO automatically creates new DAI whenever new collateral is deposited and destroys DAI whenever debts are repaid and collateral is retrieved. MakerDAO only allows users to borrow up to two-thirds the value of their ETH in DAI, meaning that for every 100 DAI created at least $150 worth of ETH was deposited as collateral.1

MakerDAO can adjust the interest rates on these loans to keep the price of DAI stable and anchored to the value of USD. If the price of DAI rises above $1 then MakerDAO can lower interest rates, encouraging more borrowers to take out loans and create more DAI. If the price of DAI rises above $1 then MakerDAO can raise interest rates, encouraging borrowers to pay back their loans and reduce the supply of DAI. Effectively MakerDAO can defend the price of DAI with the ability to charge interest on the ETH it holds as collateral.2

Terra/Luna’s stablecoin TerraUSD was uncollateralized — there was nothing backing its value except market confidence. When the market lost confidence it entered a self-fulfilling death spiral. DAI on the other hand is overcollateralized and designed to automatically liquidate loans and reduce the supply of outstanding DAI to keep the value of collateral above the value of outstanding DAI. Terra/Luna was like a fractional reserve bank where the fraction they kept in reserve was zero. MakerDAO is more like a central bank that uses interest rates and a large reserve of gold to keep their local currency pegged to the US dollar.

How SAI became DAI

When MakerDAO launched it was one of the very first DeFi applications to gain significant adoption, so there wasn’t much you could *do* with DAI other than use it to buy more ETH. MakerDAO was primarily marketed as a way of letting users spend some of their accumulated ETH gains without reducing their ETH exposure — in other words, a way to go leverage long on ETH without needing an exchange.

As the DeFi casino expanded and there were more things you could do with DAI the balance of importance shifted. Instead of DAI being a tool that let user borrow against their ETH, increasingly ETH loans were a tool that let users create more DAI. There were more users who wanted stablecoins to use in DeFi trading than there were users who wanted to use their ETH as margin for a leverage long. That was a problem because there was no limit on how much DAI could be created to satisfy the demand to borrow ETH, but the demand to borrow ETH was a limit on how much DAI could be created. In order for DAI to remain overcollateralized, the total value of ETH deposited as collateral has to grow faster than the supply of DAI.

The solution that MakerDAO landed on was to offer loans against other cryptoassets in addition to ETH. The original version of DAI (where only ETH could be used as collateral) became SAI (single-collateral DAI) and the new version of DAI could be created by depositing ETH or one of the other cryptoassets approved as collateral by holders of the MKR token.3 The new price mechanism was a lot more complex: there is now a DAI savings rate as well as different interest rates and risk ratios for each of the different types of collateral. But the basic premise is similar: MakerDAO was still operating as a central bank managing the value of their local currency but with a portfolio of different crypto-reserves instead of only ETH.

Expanding the pool of eligible collateral helps increase the supply of DAI somewhat but it doesn’t entirely release the pressure. In a bear market the demand for leverage tends to diminish for all assets at the same time and the demand for stablecoins tends to increase as people sell their other assets. That means that even with multi-collateral DAI there is still a limit to the total supply of DAI and a risk of DAI depegging to the upside if too many traders are chasing too few DAI.

Stability through compromise

In an ideal world there would be an easy way for arbitrageurs to convert USD into DAI directly so they could easily create new DAI to sell into any premium as it emerged. Unfortunately USD does not exist on the blockchain which means the closest thing MakerDAO is able to use are various USD-pegged stablecoins. But this kind of arbitrage is an awkward fit for over-collateralized loans: too much collateral and the arbitrage is inefficient, too little collateral and the interest rate quickly consumes the available buffer and forces the loan into liquidation.

Instead MakerDAO launched a special service for stablecoins called the Peg Stability Module (PSM) where users can swap DAI 1:1 for stablecoins like USDT and USDC in exchange for a small fee. That makes it easy for arbitrageurs to create more DAI (by selling USDC/USDT to MakerDAO) which improves the liquidity and stability of DAI and keeps the price tightly coupled with USD. But it also means when demand for DAI grows faster than demand to borrow against ETH (or other assets) the balance of reserves in MakerDAO will shift towards stablecoins like USDC.

Stablecoin reserves are better than ETH reserves in some ways, because lower price volatility makes the system more stable overall — but they do have a fatal flaw: the most important and widely used stablecoins are completely centralized. ~$3.5B (~36%) of MakerDAO’s reserves come now from USDC, making it the single largest source of collateral (~2.5x the size of the ETH reserves). When Circle froze the USDC accounts associated with Tornado Cash to comply with the recent government sanction of Tornado Cash that threat went from hypothetical to existential. If Circle froze the MakerDAO USDC reserves, MakerDAO would likely die.

Solve all your problems with YOLO

To solve this problem, MakerDAO founder Rune Christensen proposed a drastic possible solution: sell all the USDC in the Peg Stability Module and use it to market buy ~$3.5B worth of ETH. Trading the USDC collateral for ETH collateral protects MakerDAO from the risk of Circle freezing their USDC — but it would also greatly increase their price risk to ETH. Previous ETH reserves were overcollateralized and had an indebted counterparty who was taking on the risk if reserves fell too close to the face value of the DAI. This proposal is a bit more like MakerDAO taking out a 1:1 collateralized loan and using it to take a leveraged long ETH position.

One way to eliminate the risk of MakerDAO becoming a fractional reserve bank is by abandoning attempts to tie the value of DAI to $1. If the value of DAI is allowed to drift above (or below) the value of USD then the market can adjust naturally to changes in the value of the underlying reserves rather than triggering a bank run where the treasury is emptied as everyone races to cash out their DAI at face value while it is still possible to do.

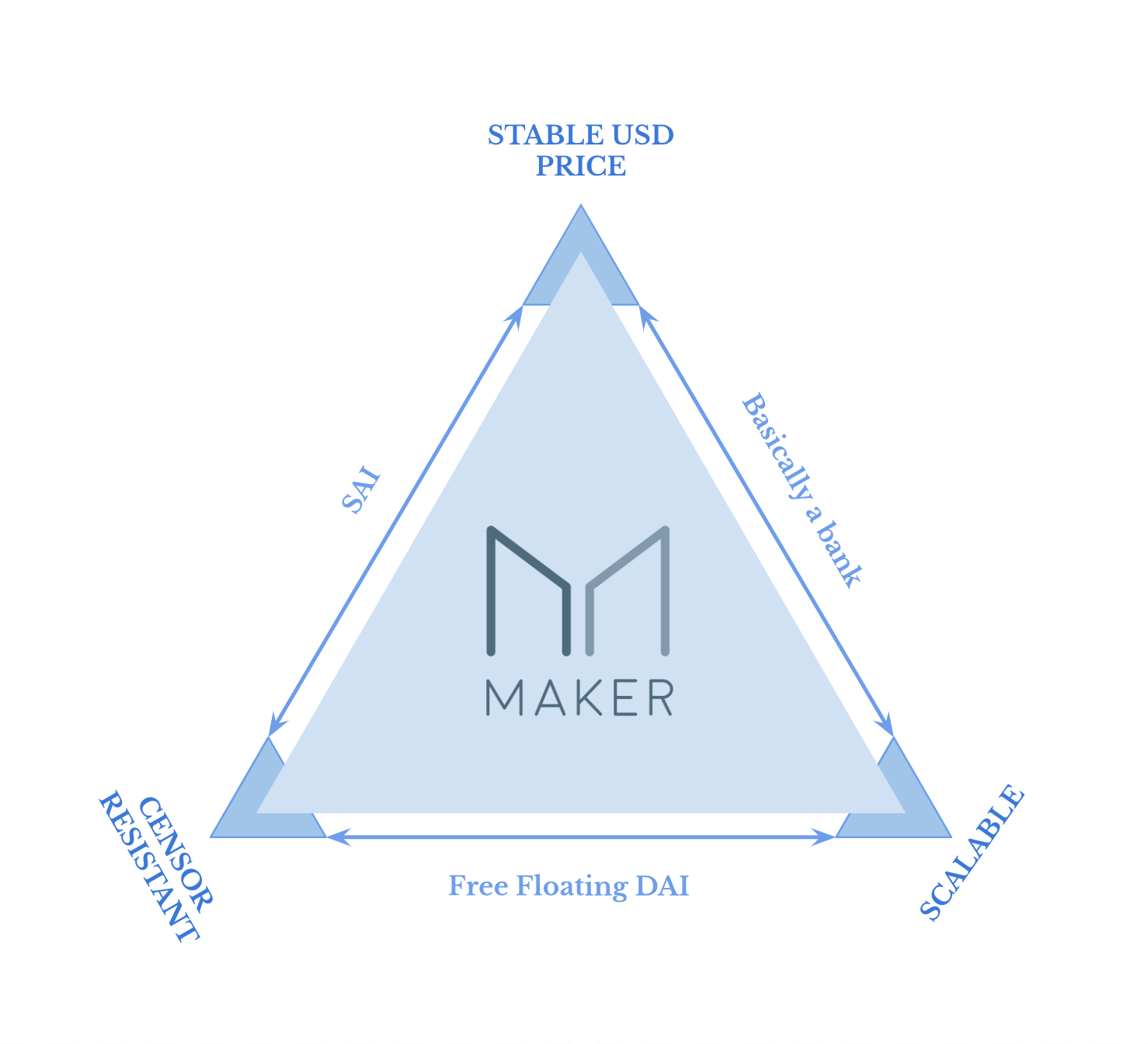

This is the trilemma that Rune was alluding to in the tweet at the top of the post: stability, scalability, censorship resistance. Choose 2.

MakerDAO can keep using USDC as collateral (letting them keep a tight USD peg and grow to a large scale but also making them vulnerable to censorship), or they can retreat back to single-collateral DAI (limiting how much they can grow but ensuring both censorship resistance and a strong peg) or they can abandon the peg to USD and let the price of DAI float against multiple decentralized assets at once similar to a modern fiat currency. DAI would no longer be stable against the dollar specifically but instead stable against the basket of assets held by MakerDAO.

Where do we go from here?

There are strong voices in favor of divesting from USDC:

And there are strong voices in favor of preserving the USD peg:

But satisfying both of those demands would require winding back to fewer or perhaps only one collateral asset and shrinking the addressable market for DAI accordingly. USDC collateral allows MakerDAO to scale to a much larger business — but if it becomes too easily controlled by outside forces it is just an expensive bank. Or perhaps an expensive-to-use-but-also-expensive-to-censor approach might be the most profitable balance. It might pay better to serve the DeFi casino than to serve the cypherpunk ideals of cryptocurrency.

As of now there are no formal MakerDAO proposals to abandon the USD peg or eliminate USDC collateral, but the debate continues. MakerDAO is one of the most authentically decentralized DeFi applications. The foundation that founded the project formally announced plans to dissolve and hand all remaining responsibilities to the DAO itself in 2021. That makes them something of an early predictor about how communities with a reasonable commitment to decentralization will balance the threat of government interference with opportunities for profit.

It’s often taken for granted that a truly decentralized community and application will be censorship resistant — but that’s a design property specific to the underlying protocol, not necessarily a requirement of every application built on top of it. It may turn out that the majority of DeFi communities are tolerant of certain categories of government censorship — either because there is broad ideological support for excluding certain parties or because there is a practical willingness to trade off censorship in exchange for access to certain markets.

The Merge is forcing the Ethereum community at large to confront the threat of government censorship and the real cost of decentralization but even if Ethereum itself manages to resist government encroachment that doesn’t guarantee the apps built on Ethereum will do the same. The choices MakerDAO ends up making will tell us a lot about what is likely to come next.

Crypto projects are like mediocre sci-fi in how they compulsively give things code names for no particular reason other than they think it looks cool. I’m going to sidestep jargon as much as I can for simplicity, but for the curious each of these individual loans is known as a collateralized debt position, or CDP.

In Maker the interest rate is known as the stability fee.

Loans in the multi-collateral DAI system are known as vaults.